The Carry Trade strategy is widely known and used, especially among institutional investors. It consists of borrowing in a currency with low interest rates to invest in products denominated in currencies with higher yields. For example, a global investment firm could finance itself by issuing 10 year Yen denominated bonds at 0.70%, exchange the currency and invest in 10 year Italian bonds at 4.35% or in a Pharmaceutical US stock with a 6% dividend yield. It is quite a cautious strategy that works thanks to different cash flows. Another interesting point is that the currency being sold – which has a low interest rate – also has fundamentals that tend to make it depreciate against the counterpart, thus also resulting in the possibility of outright capital gains.

CHF and JPY have historically been currencies with the right characteristics for this purpose: a robust and confident economy, low interest rates compared to other advanced economies, and a sufficiently large financing market. What usually happens is that in times of risk-on, with stock markets (but also commodity or bond markets lately) on the rise, investors sell suitable currencies to put their money to work on riskier assets: when market confidence fails causing a fall in risky asset prices, short positions are closed leading to a rapid appreciation of their valuations, making them behave like safe haven assets.

But there seems to have been a clear preference for the JPY lately in this respect: both USDCHF and USDJPY had risen convincingly since the end of 2020, after the Covid crisis, confirming the rally underway in the risk markets. However, the last leg up in the world indices (which started in October 2022) only saw the Japanese currency depreciate while the CHF went back close to statistically high levels for the last decade.

This is where the Swiss central bank, the SNB, comes in, as it has decided to fight inflation stubbornly above its target through direct interventions in the markets: throughout 2022 it sold foreign currency reserves (mainly EUR) to hedge against the disinflationary effects of a strong Franc (UBS estimates that in Q322 alone it conducted purchases of 3.5 billion CHF). Analysts expect this trend to continue in 2023 (total foreign reserves are close to 900 billion CHF). In contrast, in Japan, BOJ’s Ueda believes that inflation is likely to slow back below 2% in the middle of the current fiscal year and has been rather dovish on more than one occasion (talking about quantitative easing and yield curve control).

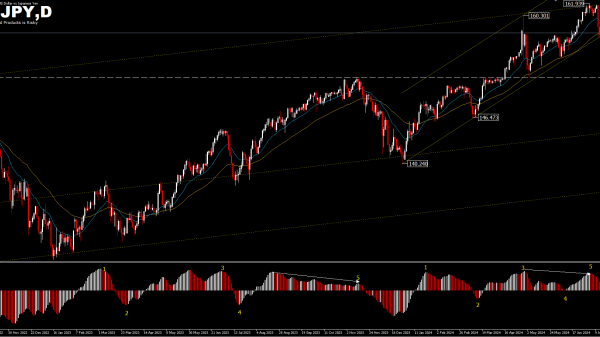

All of this has created a situation where the CHFJPY cross is at its highest since 1979 (154.35) as investors clearly prefer to sell the Japanese currency (that btw has a negative rate differential versus the Franc). It is very interesting to see how the cross behaved during risk off events: the substantial drop this year occurred in conjunction with the US banking crisis and the bankruptcy of CS; in 2022, which had been a negative year for indices and stocks, the greatest decline in the CHFJPY took place between April and May – just when the equity fall was strongest – and in December – when the market was again in sharp decline. In short, what we can deduce is that as long as the prices of indices and stocks remain biased to the upside (and the monetary policy frame remains the same), the current trend that favors the CHF over the JPY will continue; in times of greater risk instead – in which investors flow towards USD as well – it is probable that they will prefer to sell some CHF, instead of the already heavily sold JPY.

Technical Analysis

Lately there has been some turbulence on the CHFJPY cross (in parallel with the indices at their highest levels for the year) which – once it hit the 153.70 area – retreated to its 2022 highs in the 150 area (before being bid again). MA, Trend, Momentum all show the same picture: positive. Both RSI and MACD are diverging, albeit very little. The references here are the current highs (153.60 – 154), then the more steep bullish trendline (now passes around 152), finally 150.50 and last summer’s highs at 149.50. For a pullback to occur, we should most likely see the same to happen on global indices: as long as they continue to grind higher, so should the CHFJPY.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.